Mike Michalowicz 00:00:00 You don’t have to be less profitable to grow. You just have to find a way to grow that doesn’t require money. And that’s the key. Because when you have to grow without money, that means you have to be innovative. And when you’re innovative, you’re challenging industry norms. When you’re challenging industry norms, you’re the rule breaker and you’re redefining the industry.

Maureen Hermann 00:00:20 Welcome to the Group Practice Exchange podcast, where we talk about all things related to group practice ownership. I’m your host, Maureen Hermann. This episode is sponsored by Therapy Notes. Therapy notes is my favorite EHR, and it’s one that I’ve been using in my own group practice since 2014. They’ve got everything you need to be successful in your group practice, and they’re constantly making updates and have live support. If you want two free months of therapy notes, go to Therapynotes.com/r/thegrouppracticeexchange.com.

Struggling with your practices finances? Let me tell you about Green Oak accounting. Green Oak is the industry leader in mental health accounting, and they know exactly what it takes to help your practice thrive, especially when you’re scaling up.

Maureen Hermann 00:01:11 Green Oak is set apart from the rest by their deep industry knowledge and top notch advisory and CFO services. Plus they offer traditional accounting services like bookkeeping, tax prep, valuations and so much more. Here’s what’s in it for you: peace of mind, financial clarity, and the potential to significantly grow your practice and profits. In fact, Green Oak has the most impact with practices looking for financial guidance when leveling up thanks to their CFO services. And they’re not just about crunching numbers. They also offer a mix of resources like the therapy for Your Money podcast, The Profit First for therapists book, and self-guided courses to keep you informed and empowered and growing your practice. Ready to transform your practices financial health visit greenoakaccounting.com/tgpe to explore all that they have to offer. Green Oak accounting your partner in financial prosperity.

Hey everyone! Today I have the author of the Profit First book, Mike Michalowicz with me. Hey, Mike.

Mike Michalowicz 00:02:21 Hey, Maureen.

Maureen Hermann 00:02:22 How are you? I’m doing good. How are you?

Mike Michalowicz 00:02:24 Good, good.

Mike Michalowicz 00:02:24 Thanks for having me on your show.

Maureen Hermann 00:02:25 Yeah. Thank you. I know there’s going to be a lot of excited people to hear this episode, so I’m really excited about that.

Mike Michalowicz 00:02:31 I’m excited. You’re excited that they’re excited. I mean, this is exciting.

Maureen Hermann 00:02:36 So I really want to just be able to talk to you a little bit about obviously the prophet first system and some questions that myself and some of the members in my community have when it comes to our specific type of business and what we do. So we are all therapists that are group practice owners. And so I know that it can be a little bit different than some of the other businesses that you work with or that you talk to. So given that I sent you earlier a profit, first, the assessment of one of the group practice owners, that’s a part of our community, and I figure we can use that as our template to kind of discuss what that looks like and any thoughts that you have about that, as well as I’ll kind of throw in some questions that people kind of gave me to ask you throughout the process.

Maureen Hermann 00:03:30 Awesome.

Mike Michalowicz 00:03:31 That’d be great.

Maureen Hermann 00:03:31 That’s perfect. Cool. So do you know just in looking at the assessment it looks like it looks nice and clean. And I know it took me about three hours to figure out how to do it. Just because I’m not financially business savvy in that sort of sense. And I think a lot of group practice owners would say the same thing. We’re really good at people skills and counseling, and we’re always, you know, our thing that we’re always working on is like the business side, especially the financial side. We’re social workers, so we’re not taught about money or to like money or to look at money. So this has kind of been an interesting shift in doing the profit first method. And I know that those of us who started around January February have gotten to do a couple of quarters now, and it’s really fun and exciting. So it’s kind of a shift. So when you look at these assessments, do you notice any common issues that people have when completing these? Because I know a lot of people ask questions on, I can’t even figure out how to get started with this.

Maureen Hermann 00:04:27 It just seems so overwhelming.

Mike Michalowicz 00:04:28 So looking at it really, I see a couple of questions that come to mind. This may be 100% right, but there may be some tweaks. So as I’m looking at and will hopefully the people listening to this podcast can see the assessment too. Is that true?

Maureen Hermann 00:04:41 I can actually link to it. Yeah okay. I will link to it at the bottom.

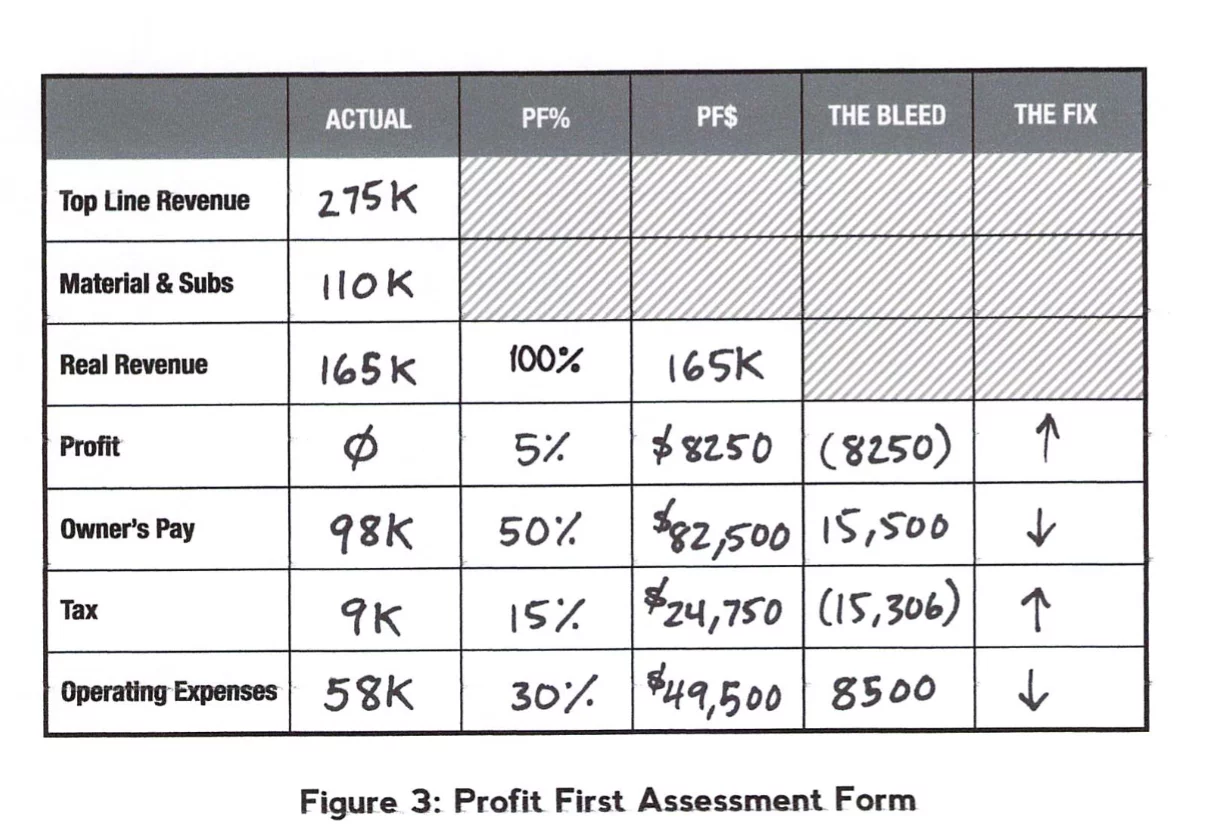

Mike Michalowicz 00:04:45 So I’ll explain some of the stuff, assuming that they don’t see it right now. And then with they have it even easier. But yeah, in the in the top sell we call it top line revenue is in the actual column. This is what the business really did. And it says 275,000 revenue. That’s perfect. So that one I assume is 100% accurate. And the good news about the profit first assessments when you’re analyzing a business, maybe the real number was 274.6. Yes. We don’t need that degree of accuracy okay. The whole goal of the instant assessment is to understand where our business has stood historically in profitability and other components of our business, and what actions do we need to take immediately to improve the business.

Mike Michalowicz 00:05:28 So even if the numbers are off, sometimes by 10 or 20%, we can still get the exact results we need.

Maureen Hermann 00:05:35 So really?

Mike Michalowicz 00:05:36 Yeah, specificity is not necessary. We just want to get close enough. I have a.

Maureen Hermann 00:05:40 Question to that really quick. I personally when I did this because I am a growing a lot, I feel like every year or two I’m either moving into a larger space or I in November, added a second location and hired, you know, seven more therapists and I’m looking into a third location every year is like the income is never like the previous one. So I did by month doing it by my average month, the past like six months. Because my income is pretty, it’s stably grows. It never really it never goes down. Is that okay to do to like get a good sense versus doing a year? Because I feel like last year looks nothing like this year.

Mike Michalowicz 00:06:21 Yeah. I see you’re saying you could use a current month, but you do have to make an annualized.

Mike Michalowicz 00:06:25 Yes. Okay. That’s fine. Okay. So you can do that. And the reason we need to annualize it is that we’re going to compare it or use a chart that has annual numbers to determine our profit first managers. Perfect. So yes okay. So the sell that says 275 sounds perfect. The first kind of strange thing is this is all professional services, right. You’re providing counseling and so forth $110,000 in And materials and subs. Sounds not typical. Now, I’m not saying it’s not wrong. I couldn’t imagine spending $110,000 on materials. Right.

Maureen Hermann 00:06:59 It’s not materials.

Mike Michalowicz 00:07:00 Yeah, it’s probably a subcontractor. So that’s a possibility.

Maureen Hermann 00:07:03 Yes it is.

Mike Michalowicz 00:07:04 Okay. We’d be clear what a subcontractor is. Okay? A subcontractor is someone who works for our business on needed basis. The work they derive for us is to the benefit of delivering our services, typically meaning it’s not a graphic designer. It’s someone that helps deliver the end service to my client. And they have typically their own business. Yeah.

Mike Michalowicz 00:07:27 So my favorite example that makes it clear is if I build homes and I do $275,000 in revenue building homes, and I have $110,000 of subcontractors, that’s likely the plumber who does the puts the pipes in and the electrician who puts the wiring in, and the other contractor who puts the sheetrock up. Those are subcontractors, meaning they don’t just sheetrock for me, they do it for someone else. Right? The guy that owns the electrical shop, it’s his shop, his liability. So they’re own independent businesses and they’re all delivering a service that is of an end benefit to my customer. It’s a new home. If one of the people was an advertiser who makes brochures to market the houses, they are not a subcontractor. Yes, they own their own business. Yes, they can work for others, but the work they’re delivering is not for the end benefit of the customer. It’s just for promoting my business.

Maureen Hermann 00:08:20 Right? Operating expense. Yeah. So this question comes up a lot, even outside of the profit first system with our business as group practice owners, is whether we should have 1099 independent contractors who own their own business and who are providing counseling services in our practice or having W-2 employees.

Maureen Hermann 00:08:40 So it’s kind of I’d say like 75% of group practice owners have employees. I have employees as well. I know this person right now. They’re independent contractors. They do have their own business and I know in our field it is a little funky because it’s not so much like with home building where the painter comes in and he’s truly being contracted out and he paints for, you know, 20 other companies. But I know this person is also in the process right now of switching to W2 model. So the ten 110,000 is for his independent contractors, but they will essentially be employees in the next couple of months. I know he’s in that process, but in terms of pay difference, typically in our field we reduce by around 10% to give for the tax absorbent malpractice insurance that we have to cover then. So the 110 would still be around 110 as W-2s. But maybe we’re putting it then in the wrong category.

Mike Michalowicz 00:09:33 Right? Right. So if their employees of your company 110 goes to operating expenses.

Maureen Hermann 00:09:38 That’s how I do it.

Maureen Hermann 00:09:39 Which is why I was initially at emailed you, because my percentages look so different than what’s on your thing. I do 82% of operating expenses. 66% of that is to my employees, and only 10 or 11% is actual, you know, expenses.

Mike Michalowicz 00:09:54 Yeah. And that we see that far more often in a service based business, like you have to offer that there is no materials and subs. And that’s why I kind of raised that red flag for me that have 110 up there. But I understand it. And the next row down says real revenue. So it shows $165,000 in this case. Why we have this real revenue is that represents the revenue the company truly or really is making. It really generates $165,000 in revenue. And then it’s basically transferring money from clients over to these subcontractors to the tune of 110,000. Yes. I mean, literally the client’s saying, here’s a check and say, oh, okay, this check is for so-and-so, so I’m handing it over. So we make this adjustment to say, you don’t have a $275,000 business, so don’t act like that.

Mike Michalowicz 00:10:42 You have $165,000 business. Let’s act just like that. Right? So that’s why we do that adjustment. The next cell down says profit. There’s zero profit. That’s very typical. it’s very infrequent that a company will be paying a profit distribution above and beyond what the owner takes in pay. So I expect that to be zero. I don’t want it to be zero, but I expect that to be zero. And when we go into the adjustment columns, we’re going to start reserving money for profit. Next thing is the owner is taking nearly $100,000 in pay, which that makes sense. When we do the assessment, you’ll see we’re actually suggesting a slightly lower compensation to the owner. Why is that? When the owner takes as much as possible. Right. Yeah. What we do, but not as pay because what we found is people adjust their lifestyle to match what regular compensation they take. So if a person takes home $100,000 a year, most people will live a $100,000 lifestyle. And the second some kind of anomaly happens.

Mike Michalowicz 00:11:42 They’re in real trouble. We maximize our life to the last penny we’re taking home. So we want to take home as much as we reasonably can to live comfortably. But we want the business to have reserves for the other necessities in life. So that’s why in this case, we do this analysis. We’re actually suggesting curtailing the compensation by about 15,000 bucks. Next count is tax. The tax count. This business has had $9,000 in taxes that the business paid. I’m also suspect of that. I’m not saying that’s wrong. It’s quite possible. But for most businesses, the business doesn’t pay any of the taxes. The owner, in fact, is paying the taxes themselves. It comes out of their personal pay. So what this person is saying is that the business actually paid the taxes to the tune of 9000 for them. So I just question if that’s true. Okay.

Maureen Hermann 00:12:32 I can talk with him about that. And see, I know that a lot of us in our line of business do pay some portion of it based off of our previous year’s estimated income they give you, you know, the estimated income.

Maureen Hermann 00:12:45 I know a lot of us pay through our business that amount. But what I do notice is that almost 100% of us at the end of the year, because we’re constantly like a growing business and hiring more employees and stuff, end up owing a whole lot more. And then that left over, like I did this last year before I read your book, I, you know, paid my estimated taxes through my business. But then at the end of the year, because I’m an S corp, it could, you know, we do our taxes altogether. I pay then personally the extra, you know, 12,000 that I owed or whatever through my personal side. So this is you know, since reading your book a shift that I’ve done as well to really make sure that all of the taxes just get paid through the business. Love it. Love, love me too.

Mike Michalowicz 00:13:23 Yeah. So and then the last account is the operating expenses. This owner says it’s 58,000. What I would do then is I would add up all the cells that are filled in for profit, which is zero owners pay, which is 98.

Mike Michalowicz 00:13:37 In this case tax, which is nine operating expenses, which is 58. And make sure it matches real revenue. So just eyeballing it looks like it does. And that means we have a balanced assessment here. The next column is the percentages. Now these percentages that we see for profit. It says 5% owner pays its 50% tax 15% and operating expenses 30%. That is just a copy and transfer. I did a analysis of about a thousand companies, a study of a mixed companies, everything from pizza shops to psychotherapists to, you know, lawyers and accountants to manufacturers. And instead of saying, what’s the industry average for an industry? I simply asked, what do the fiscally elite do? A different question, you know, what do the healthiest businesses achieve based upon the size of the business? And what I did was I looked at the company’s real revenue, the revenue it actually generates, in this case, this business was 165. And so when a business is at 165 K, what is the percentages that a really fiscally elite company would be allocating money to these purposes.

Mike Michalowicz 00:14:46 So that’s how I got these percentages. And the percentages are for range sizes. So I think I did businesses under 250,000, businesses 250 to 500,000 and all the way up to 50 million. Yeah. The important thing about these percentages, these are called Taps, stands for target allocation percentages. I’m triple underlining the word target. That does not mean a starting point. It’s simply what we’re targeting for the future. I also want to note that in small businesses in particular, some businesses will actually be outperforming those numbers and say, wow, I’m doing so great. Everything’s fine. That’s not necessarily true. These numbers are simply what the fiscally elite typically do. But in some, especially for some smaller businesses, if you’re doing better, that just means that congratulations, you’re among the elite right now, but you can still do better. You can still ramp it up. So don’t think that you should ever slow down your business’s performance, that said that’s a mistake. Yes. So okay, so I look at this analysis and in this case this is pretty typical.

Mike Michalowicz 00:15:45 The analysis says, you know, you’re putting no money toward profit. The fiscal elite put 5% there. You should be allocating $8,250 toward profit annually. So we need to increase our profit contributions. The owner’s taking 98,000. And in this analysis, an owner of this size business would do about 82,500. They’re taking a little bit much. So we’re going to allocate less money to paying them decrease their annual compensation by 15,000, which when people hear that they have a heart attack and say, you can’t take a penny from me. And my response is, well, then grow your business more, but you’re taking too much to allow the business to be healthy. And that’s dangerous. Like you’re actually crippling your business by taking how much compensation you do based upon the size of your business. So either adjust your income so the business can be healthy or make the business stronger and bigger so it can provide you that income going forward. So I have.

Maureen Hermann 00:16:39 A question with that, which is one of my bigger questions that people were asking is how do you give in all of this if you want to grow, how do you know financially, looking at this picture when it’s a good time to grow? And how do you do that with the profit first method to make sure that in our business, again, we don’t have a lot of costs like to grow would potentially mean having another location.

Maureen Hermann 00:17:06 And most of us don’t buy locations. We rent a couple thousand dollars a month to have, you know, 4 or 5 offices, and then we have to furnish it, you know, with couches and chairs. We usually just, you know, sit and talk. So it’s a maybe 10 to 15,000 to furnish a five office suite. And then we’re done. We then we have to hire people. And in our case, we don’t pay employees unless they bring an income. So we never have to pay before we make the money as a business. So there is really kind of a low risk on that end. So how do we use this assessment or look at this, or go through this prophet first and then know and implement it right when we were trying to grow. Like I know his goal here says he wants to get to 500,000 in the next two years. And of I think that’s his top line revenue. What he’s thinking of 500,000, I don’t think real. And then to have six more or higher, 3 or 4 more therapists.

Maureen Hermann 00:17:56 So I guess what were you saving it and then the operating expenses or do you can you keep the profit? I know you say don’t use profit for anything but profit.

Mike Michalowicz 00:18:04 So yeah. So this is the biggest challenge I get with profit first people say, but Mike, how do I grow if I take profit? And I don’t know who on this planet said that profit and growth are polar opposites, I don’t know who said they’re a dichotomy, that if you want to grow, you can’t profit, or if you want profit, you can’t grow. But whoever put that out there did a good job because everyone believes it and it’s total bullshit. It’s a total freaking lie. And it’s a shame. And now I’m spending, I think, the rest of my life trying to unwind that misnomer so you don’t have to be less profitable to grow. You just have to find a way to grow that doesn’t require money. And that’s the key. Because when you have to grow without money, that means you have to be innovative.

Mike Michalowicz 00:18:46 And when you’re innovative, you’re challenging industry norms. When you’re challenging industry norms, you’re the rule breaker and you’re redefining the industry. So the goal here is to think outside the box. That’s what Profit First does. And we now have I mean literally thousands of companies that we have documented doing profit first. And we believe there’s about 30 if not 40,000 companies now actually doing profit first. But the documented cases we get consistently, the companies that focus on profit first outgrow their competitors faster growth in the question, of course, is why is it? Well, when you focus on profit, you have to work and you deliver only the services that are profitable. So you have to start curtailing non-profitable services. And when you start reducing your service set to be only profitable, you will start introducing less services, which means you have to be more focused on the client base you serve. You have less variety in your offering. That means you’re going to have less variety in the clients you serve. So now you have fewer products for fewer variety of customers, which means to serve them, you need to have the most elite services.

Mike Michalowicz 00:19:50 And if you have the most elite services for a narrow sect of people, that’s called niche focus and niche specialization, which, by the way, is the fastest growth method out there.

Maureen Hermann 00:19:58 Yeah, we do that totally.

Mike Michalowicz 00:20:00 Yeah.

Mike Michalowicz 00:20:00 So because people in the niche will say, you got to go to Maureen. She’s like the best. So they actually start the automatic marketing for you. There goes your marketing costs, customers handling it for you automatically. And because it’s your most profitable products, your profit increases. So the growth and profit go hand in hand. So whenever someone says, you know, I don’t know how to grow now because I’m focusing on profit, my question is you’re not thinking enough. How do you grow without putting money into it? How do you become famous among your customer base so they want to market for you? How do you look at the standard industry norm of you gotta have another office or you gotta lease it and do something that no one’s ever done and change the rules of the industry.

Mike Michalowicz 00:20:39 That’s how you approach it.

Maureen Hermann 00:20:41 So how do you do it then from like the financial perspective, where are you taking it from the so not profit I know. But then operating expenses like the left over that’s in.

Mike Michalowicz 00:20:50 There thinking what money for to do.

Mike Michalowicz 00:20:52 What to.

Maureen Hermann 00:20:52 Start the second location.

Mike Michalowicz 00:20:54 Yeah. So first of all my question is how do I do this without spending any money. That’s step one okay. Step two is if I gotta spend some money, where do I find it? Absolutely. In your operating expenses, you have enough operating expenses. That means your current business is not big enough to support that growth. We gotta get more revenue coming in. So filter down.

Maureen Hermann 00:21:10 Okay, that makes a ton of sense. I think people were wanting to take from the profit. Oh, don’t. Right, right. And I after reading your book I’m like I went from not taking profit to taking profit and not looking at it until the quarter ends and taking it, taking my 50% of it.

Maureen Hermann 00:21:26 And that’s mine. Not using it towards the business or anything else. But I think, you know, people were trying to figure out their very, I think, in our industry. And it might be just common among people as a whole are very black and white thinkers, and they want to follow the rules. And so they’re like, If I’m doing this, where do I take it from? Literally, you know, because it costs us some money to open up another location. But now it’s I think it’ll make sense to people that they can use what’s left in the operating expenses if they’re actually making more than their location allows for it, then they have extra, you know, leftover operating expenses. They can use that.

Mike Michalowicz 00:21:59 And I do want to challenge that because I think you’re falling into the belief of, well, it does take some money to open a location. Really? Who said that? And I’m not trying to be a schmuck here. I’m just trying to drive home. The point is that we follow the normal belief and therefore we follow that pattern.

Mike Michalowicz 00:22:12 But what if we get a space that’s performance based? We find a landlord says, I’m moving in, I don’t have the space can perform, but I’ll give you a percentage of the revenue as it comes in from this space. Maybe someone will take you up on that.

Mike Michalowicz 00:22:22 Yeah. I mean.

Maureen Hermann 00:22:23 We get you.

Mike Michalowicz 00:22:24 Yeah.

Mike Michalowicz 00:22:24 So that’s that. But it does come out of operating expenses if you need to spend money.

Maureen Hermann 00:22:28 Okay. Perfect. I’m sorry I cut you off on that whole piece. As you were going through this, was there anything you were finishing up on at the bottom? You were on operating expenses with, like, the bleed?

Mike Michalowicz 00:22:38 Yeah, yeah, the percentage is. Oh, so the last part is the bleed. So we do this analysis, we see that the owner’s pay should be 82 five as opposed to 98, the tax reserve. And this is the most common thing I see. The taxes are far short. Yes. So this business paid $9,000 in taxes for the owner, which is more than most businesses.

Mike Michalowicz 00:22:58 Most businesses pay zero. But really this business owner shared the business allocating and reserving $24,000 in taxes. Because think about it, this owner’s taking home $82,000 plus another bonus on top of their profit at the end of the quarter that accumulates over the year to $8,000. So they’re taking home 90 plus thousand dollars in the model. When you take home $90,000, your tax bill at the end of the year is not $9,000, right? That’s a 10% tax. It’s more like a 30% 3% tax or 35%. And if we take 90,000 times, let’s say 30% for round numbers sake, that adds up, I think, to $27,000. Well, the business is reserved 25,000 in this example. So it’s almost there. These percentages aren’t perfect, but it’s almost there. So right now I can tell just by looking at these numbers what the owner experiences. And the year comes tax bill do is due in the owner goes, oh I don’t have enough money. how am I gonna pay these taxes? I need to borrow some money or, and there’s kind of this panic mode, and we want to get out of that reactionary panic mode and just have the business reserve for the tax liability up front.

Maureen Hermann 00:24:07 Yeah, I completely agree. I think the one thing that comes up the most between, you know, January and June is them realizing that they owe taxes on the previous year and hadn’t saved up for it. And then, you know, ask the IRS if they can have a payment plan and then that passes into the following year’s worth of. Yeah. Oh, I know, it seems so messy. So it’s what’s really great is, you know, if you figure out how to implement this the right way, that saves you all of that time, aggravation, money at the end of the year to come up with it for the taxes. Yeah. Yeah.

Mike Michalowicz 00:24:41 Yeah. Exactly. Well, and the last thing is the operating expenses. So we need to reduce operating expenses. And this is a very common almost every business we analyzed needs to reduce expenses. So in this chart we see a business going from 58,000 down to just shy of 50,000. So about an $8,000 cut in expenses. And we see this in most businesses.

Mike Michalowicz 00:25:01 Most businesses are spending just too much money. Cutting expenses is pretty easy for most businesses, to the tune of about 10 to 15% of their total spend. It’s pretty easy to say, oh, we don’t need to have that third phone, we don’t use it and we cut these things. At certain point. You can over cut expenses where you start cutting into the muscle of the business where you know, well, if I got rid of that employee, there goes a big expense. But also that employee is running our entire business. That would be crushing. So you can’t get rid of an employee, so to speak. So cutting 10% is easy for most businesses. And I think that’s where we start. Sometimes businesses cut more, but also we want to look to increase margin. So many people think profit first is about cutting costs only. And that’s actually the minority of it. The increasing margin is the bigger, greater opportunity where we say what other services or products can we offer at a premium so that our margin, the amount of profit per product, increases dramatically.

Mike Michalowicz 00:26:00 So for this business, I want to look at both how we cut some obvious costs and how we increase margin.

Maureen Hermann 00:26:05 Awesome. And I think that’s something that people in our industry are starting to get creative with. Because when we are doing counseling, we really kind of are narrow minded in our focus of one on one counseling. And that’s all there is. Insurance pays X amount for it, or you can charge only X amount per hourly session of counseling. but I’m noticing in the past few years that people are getting creative of. You know, offering continuing education to other therapists where they can charge more, or, you know, doing workshops or running groups which allow for more income in a given hour. So I get what you’re saying with that. And I think that’s in our industry, some of the things we might need to be looking at, aside from niching ourselves down as much as possible.

Mike Michalowicz 00:26:48 Yeah, I agree fully.

Maureen Hermann 00:26:49 So I want to just move this for this last little piece to how we can, because you have a little bit at the end of your book on how to make it work.

Maureen Hermann 00:26:57 On the personal side, I know a lot of people were having questions from, you know, how do you apply the percentages and all of that. And I know you have the, you know, income, the vault, the day to day debt destroyer, I think, and then recurring payments. But I think people are in our industry again, very black and white thinking need the steps. How can we really implement this in a good way? And our personal side, when, you know, people have a lot of these fixed things like, you know, mortgages and debts that will always be there. So it’s not we’re not able to like, you know, mortgage. We’re not going to be reducing that until we’re pretty much retiring.

Mike Michalowicz 00:27:37 Yeah.

Maureen Hermann 00:27:38 Or health insurance or retirement accounts. Like where does that all fit in in this for you.

Mike Michalowicz 00:27:43 Yep, yep.

Mike Michalowicz 00:27:44 So this is, ultimately the system is nothing new. I didn’t invent anything here. I think I’m the first person that says that said that this system, which is called the envelope.

Mike Michalowicz 00:27:53 System.

Mike Michalowicz 00:27:54 I said it applies to business. Right. So that was kind of the Like, businesses can do this when it comes to our personal life. It’s the envelope system, something that’s been tried and true and literally around since BC. There’s a book called The Richest Man in Babylon. It refers all the way back to BC, when this system was used, and the idea was instead of having money in one spot in a lump sum, that we instead we allocate it to a purpose so we know what purpose that money is meant to serve Right before it actually gets spent. So what we did in our business, here at our business, we set multiple accounts. A profit account is the purpose of profit. The owners pay is to pay the owner as its purpose tax to pay tax operating expenses to pay the expenses of the business. In our personal accounts, I found we have to allocate or create accounts for these different purposes. So I have in my own personal account, I have a mortgage account and every time my money comes in, it flows my business from my owners pay, right? That’s what pays me.

Mike Michalowicz 00:28:48 It goes into my personal income account. It’s what’s called. Then it gets divided into its envelopes. The mortgage envelope. I have a vacation envelope. I have my wife and I, we actually have our own debit card accounts. Her name is Krista. Chris’s debit account, Mike’s debit account. And that’s for, like, little miscellaneous stuff. When I go out and need to get some hammer and nails at Home Depot to do some work on the house this weekend, it comes out of my debit card when she goes, you know, food shopping for dinner tonight comes back from Wegmans or new favorite store. When she comes back from Wegmans, that debit card is being used. Our children’s college accounts. We have one for each child, and then that in turn gets transferred to a 529 plan. So what we have to do is create accounts for all of the significant expenses. I’m not saying for every expense you don’t have, like a cable TV account, a telephone account. That’s that’s.

Mike Michalowicz 00:29:45 Crazy.

Mike Michalowicz 00:29:45 It’s crazy.

Mike Michalowicz 00:29:46 I found for most personal lives, somewhere between 5 to 10, maybe 12 accounts is enough. In my business, I find somewhere between 5 to 8 accounts is enough. Maybe 9 or 10. So in the personal life, I have a few more accounts. Like for an automobile, for example. We own our automobiles, we buy our cars, and we’ve paid them off. And but we still have a monthly installment going to an automobile. Not that we’re paying for one, but when I’m ready to buy the next automobile, it’s a purchase for cash. So there’s money going to the automobile account every single actually 10th and 25th. So twice a month money’s going in there accumulating. And then once I hit the number, I can just look at the count and know what size or expensive car I can afford. And then I’ll decide one day, okay, now I’m ready to buy a car and here’s the top line I can spend on it. What do I really want to spend? So that’s how it works on our home front.

Maureen Hermann 00:30:40 So is there any method that you use to figure out like how? So I am not doing it fully on my personal side because I’m honing in on using it right on the business end. My personal side, I think I have seven accounts like vacation for the kids, 504 or 4, three B plan or whatever it’s called. I’m thinking of the wrong one for a three B’s retirement account to their college funds. So they have calculus five, five, five. Yeah, there we go. So I have an account for that. So we have a I think about seven accounts and an emergency fund and all that. So but I think I am noticing with the questions that people were asking and I haven’t yet figured this out myself, is how do you know that you’re then overspending because there isn’t these nice categories that you have in the profit first, where it says about 5% should go to this, about 10% should go to this, that what if we’re opening, you know, all these accounts because we’re over big over spenders and we have, you know, a student loan account, a mortgage account, a kid’s school account day to day.

Maureen Hermann 00:31:35 Like, what if we’re putting, you know, we’re overspending and we don’t know in one area we should not be overspending in, you know, what’s our day to day? I might spend, you know, a hundred a day in another person puts $20 a day in their day to day account.

Mike Michalowicz 00:31:48 Exactly. So that’s a great one. And that’s the spawns me or sparks the desire for me to write another book.

Mike Michalowicz 00:31:55 Yes, please.

Mike Michalowicz 00:31:56 So I will get to that one day. But in the meantime, what I found is we look at our normal, our historical normal, and have that as our base point and start there. For example, if I want to lose weight, the first step to losing weight is to determine how much do I weigh now? So it would be a mistake for me to say to someone, Oh, if you want to lose weight, lose £50. Well, if you are a male that weighs £180 and your ideal body weight is 170. But I just told you to lose £50.

Mike Michalowicz 00:32:27 I actually may kill you or at least put you on the verge of death. So we have to look at your starting point in our personal lives. First, determine the categories, then look. Historically, what have you spent as a percentage of your income and now give you your starting percentages? You know, my mortgage is I don’t want to take in $10,000 a month, I’ll say, and my mortgage is normally $1,000 a month. Well, that’s 10%. So my starting point is 10%. Then my goal is for improvement. Now mortgage won’t change, but my income can change. And I could say ideally I want to get my mortgage down to 7%. And so therefore the only way to do is I need to increase my personal income for that number to work. So look at your historical determine where you are and then determine what you want to target. And unfortunately, I don’t have those numbers for you because I haven’t researched or prepared for a book like that one yet. But that’s at least how I get started on this process.

Mike Michalowicz 00:33:22 And I think.

Maureen Hermann 00:33:22 If we did that, we would be able to see where we feel like we’re spending too much. I don’t think it’s too hard to be like, okay, well, on food and eating out out of the 10,000 that I make in a month, I’m spending 3000 of it on food and going out and not cooking at home. And, you know, unless you’re not spending money anywhere else and that’s all you like to do is eat out, maybe that’s fine. But other people like myself, if that was the case, I might realize, okay, I think I can, you know, really reduce that to still be able to go out to eat, but maybe not three meals a day every day anymore and, you know, twice a week instead.

Mike Michalowicz 00:33:58 Yeah, that’s exactly right. That’s exactly right. You can do a self-assessment, and we just have to be just honest with ourselves. Yeah, just be totally honest with ourselves. And if you are, you’ll see where the opportunity is.

Mike Michalowicz 00:34:09 And the goal is to make these improvements incrementally and not one fell shot. So instead of saying I eat three times a day right now or whatever it is, and based upon this assessment where I want to be, I should be out once a week, not, you know, 21 times a week. To make that jump over is such an abrupt change to our behaviors that our likelihood of a failure rate is much higher. But instead of eating out 21 times a week, three times a day, if I ate out 15 times a week, I still can go out every single day. But now it’s two meals a day. It may not be as negatively impactful on my behavior. And then we ratchet down from 15 to 7, 7 to 3, and then ultimately get to that one over time, but just go in increments.

Maureen Hermann 00:34:52 Yes, I agree, I have noticed people who are starting to profit first in our community getting really excited about it and then just really wanting to dive right in. Yes, you know, I can understand and appreciate that going that route will likely lead to failure or, you know, pulling from the profit account to pay for this because you you just did too much at once.

Mike Michalowicz 00:35:13 Exactly.

Mike Michalowicz 00:35:14 And that’s actually, you know, the first person I think I know actually, on this plan to do private first was me, because I’m the guy who wrote the book. So I set the system up for myself. And listen, I’m not saying I’m the first to do a system like this. These systems existed, but this version or this flavor I did for myself first, and I noticed how excited I got. I was like, this is it. I found the formula. I’m gonna throw 50% profit, I’m gonna get rich this way. And it was such an abrupt change that the system failed because my business couldn’t support it, my lifestyle couldn’t support it. And then I said, well, clearly the system sucks. This will never work. This was the dumbest idea ever. I can’t do this. And then I said, hold on one second. I’m going right back to the workplace. I was let me start again. So going all in is exciting and it feels like the right choice.

Mike Michalowicz 00:36:00 But I’ve seen it hurt businesses, including my own. I’ve now and very quickly it’s just to say I got to go and slowly and consistently because I need to be there persistently and that’s what’s worked for me.

Maureen Hermann 00:36:11 I love that, I love that statement. So I don’t want to keep you any longer. But was there anything else that I either didn’t ask that you think is useful to know? Or do you feel like I’ve kind of touched on everything? Gotten you to touch on everything I should say?

Mike Michalowicz 00:36:22 I have talked to you.

Mike Michalowicz 00:36:23 I’ve never done an incident assessment on a show like this before. I think that’s a genius idea. I hope it gives people good insights. My one final tip is if you haven’t started Profit First yet, to get started to set up one account, like the idea of starting off slowly persists all the way to the level of setting up the accounts themselves. These are all different checking accounts. You can set up the income account, the real revenue account, the profit account owners pay.

Mike Michalowicz 00:36:49 But just start off with a profit account because anyone listening right now can call their bank and within ten minutes online or on the phone, have a one new checking account added or savings account. Then they name it profit and starting to say allocate 1% of your money. Because if you’ve never taken a profit before, why not start with 1%? It’s small enough and if you can run your business off $1,000, you can run your business off 1% less, which is $990, so it won’t have a negative impact on your supporting your business. But you’ll start seeing the profit accumulate. And when you start seeing some profit accumulate, no matter how small it is, you’ll start winning yourself over to the system and then you can build from there.

Maureen Hermann 00:37:27 That’s great. Thank you so much. I think that’s a good way to end this. And I guess any yeah, it’ll give anyone who hasn’t yet started the profit first method. I think a little bit of like umph to go do it. Mojo. Yeah. Mojo.

Maureen Hermann 00:37:41 There we go. And for everyone else who’s already doing it and literally is just all in on this, they’re just going to be super excited to hear this. So thanks again.

Mike Michalowicz 00:37:51 My pleasure. Yeah.

Maureen Hermann 00:37:52 All right. Well it was so nice to meet you and to be able to talk to you.

Mike Michalowicz 00:37:55 Likewise.

Maureen Hermann 00:37:55 Thank you. All right. Have a good one. Thanks for listening. Give us five stars on whatever podcast streaming service you use, and I’ll see you next week.